▷ Finance

Credit cards evolved from early merchant credit systems into a global financial tool, with roots stretching back to ancient borrowing practices and early store‑issued charge tokens in the late 19th

and early 20th centuries. By 1914, Western Union introduced metal charge plates, followed by innovations like the Air Travel Card in 1934 and the Charg‑It card in 1946, which allowed limited local use.

The modern era began in 1950 with the launch of the Diners Club card, the first multipurpose charge card usable at multiple merchants, and expanded rapidly when American Express and BankAmericard

(later Visa) entered the market in 1958. Technological milestones—including the magnetic stripe in 1969 and EMV chip technology in 2010—transformed security and global usability, while rewards

programs and revolving credit reshaped consumer behavior. Today, credit cards are central to everyday finance, with U.S. consumers carrying over $1.23 trillion in credit card debt and an average

balance of $6,768, reflecting their deep integration into modern economic life.

The magnetic stripe on modern cards emerged from IBM engineer Forrest Parry’s early‑1960s effort to attach magnetized tape to plastic identification cards, a breakthrough that became practical only

after his wife suggested using a household iron to fuse the materials together . IBM refined the technology throughout the decade, and by 1969—under project manager Jerome Svigals—it established the first U.S.

standards for magnetic‑stripe cards, followed by international adoption two years later, enabling global interoperability and secure machine‑readable transactions . The magnetic stripe itself drew on decades

of earlier magnetic‑storage innovation: magnetic tape had been developed in Germany in 1928 and later adapted by IBM and others for computer data storage in the 1940s and 1950s, proving its reliability and

paving the way for its use on cards . Together, these advances transformed credit card processing from slow, error‑prone manual imprinting to fast electronic verification, laying the foundation for modern

payment systems.

When someone dies, their debts don’t pass to children, siblings, or other relatives; instead, they’re settled through the person’s estate, meaning whatever money and property they leave behind—bank

accounts, investments, vehicles, real estate, and similar assets. If the estate doesn’t have enough value to cover everything, unsecured debts such as credit cards or personal loans are usually forgiven,

leaving family members free from any obligation to pay them with their own funds.

Debt collectors are legally restricted in how they contact relatives, and under the Fair Debt Collection Practices Act (FDCPA) they may speak only with the deceased person’s spouse, parent if the

person was a minor, legal guardian, executor, or administrator; they cannot suggest personal responsibility if someone falls outside these categories, and a written request to stop contact carries legal

force and requires them to cease communication.

Most relatives are not responsible for a deceased family member’s debts, and personal liability arises only in narrow situations such as co‑signing a loan, holding a joint account, living in a community‑

property state, or inheriting secured property; knowing both your rights and the estate’s obligations helps you avoid unnecessary payments and shields you from aggressive collection tactics.

An annual home budget becomes far more than a spreadsheet when framed as a roadmap for the year ahead, turning scattered expenses and vague intentions into a clear plan that anticipates seasonal

costs, major purchases, and long‑term goals while cutting down on financial surprises; it brings structure to irregular income, steadiness to family spending, and a sense of calm to anyone trying to

save or reduce debt, all while offering a wide‑angle view that makes smarter decisions feel natural rather than forced.

Preparing an annual home budget becomes a powerful anchor for homeowners, turning financial uncertainty into a clear, manageable plan. It creates space to track both predictable and surprise

expenses, building readiness for everything from routine maintenance to sudden repairs. With a thoughtful budget in place, it becomes easier to anticipate costs, map out maintenance needs, and sidestep

unwelcome financial shocks. It also sharpens long‑term goals and strengthens overall control of personal finances, making the entire year feel more intentional and steady.

In 2025, the paychecks of world leaders reveal striking contrasts, with Singapore’s Prime Minister Lawrence Wong earning an extraordinary US$1,647,000 annually, far surpassing peers and

reflecting the nation’s policy of competitive salaries to deter corruption. Switzerland’s Federal Council President Karin Keller-Sutter follows with US$553,000, while the U.S. President Donald

Trump receives US$400,000, Germany’s Chancellor Olaf Scholz earns US$396,000, and Australia’s Prime Minister Anthony Albanese takes home US$382,000. Austria’s Chancellor Christian Stocker collects

US$311,000, Belgium’s Prime Minister Bart De Wever earns US$293,000, Japan’s Prime Minister Fumio Kishida receives US$316,521, Canada’s Prime Minister Mark Carney earns US$279,000, and Luxembourg’s

Prime Minister Xavier Bettel rounds out the top ten with US$278,000. These figures highlight a vast disparity, where some leaders command salaries exceeding a million dollars while others,

particularly in smaller states, earn symbolic stipends, underscoring the diverse ways nations value leadership and public service.

In 2024, identity theft surged to alarming levels, with the FTC receiving over 1.1 million reports—cementing its place among the top consumer complaints. Once scammers gain access to personal

data, they can wreak havoc by opening credit accounts, securing loans, or filing fraudulent tax returns. Even more insidious is the rise of synthetic identity fraud, where real and fabricated

details are fused to create entirely new personas. A scammer might pair a legitimate Social Security number with a fake name and address to build a credit profile that slips past detection.

These synthetic identities often fly under the radar for months or years, enabling long-term financial exploitation across multiple institutions.

Imposter scams have surged in 2025, with fraudsters posing as trusted authorities—government agents, bank staff, or tech support—to manipulate victims into handing over money or sensitive

information. These schemes often begin with a phone call, email, or message that appears legitimate, complete with official-sounding language and spoofed contact details. The urgency is key:

targets are pressured to act fast, whether it's resolving a fake tax issue, securing a compromised bank account, or fixing a fabricated tech problem. With AI tools now amplifying the realism

of these impersonations, distinguishing truth from deception has become increasingly difficult, making vigilance more critical than ever.

Banking scams in 2025 have reached unsettling levels of sophistication, with AI-generated alerts and phishing messages mimicking legitimate financial institutions down to the tone, branding,

and timing. These scams often arrive as urgent notifications—claiming suspicious activity, locked accounts, or pending transactions—and direct recipients to realistic-looking login pages. Once

credentials are entered, scammers gain full access to accounts, often initiating transfers before the breach is detected. Some schemes even deploy AI chatbots to simulate real-time customer

support, deepening the illusion. In an era where digital trust is currency, these scams exploit familiarity and urgency to devastating effect.

In 2025, scammers have weaponized artificial intelligence to create eerily convincing deepfake videos and voice calls that impersonate executives, relatives, or officials, often demanding

urgent financial action. AI-driven chatbots and fake customer service portals mimic legitimate institutions with unsettling accuracy, luring victims into revealing sensitive data. Hyper-personalized

phishing emails, crafted by language models, bypass spam filters and exploit emotional triggers with surgical precision. By mining public data, these scams are tailored to individual targets,

referencing personal details to build trust and urgency. The result is a new breed of fraud—slick, scalable, and disturbingly persuasive.

As of 2025, roughly 92% of the world’s currency exists only in digital form, leaving a mere 8% as physical cash. This shift reflects a seismic transformation in how economies operate,

driven by credit cards, mobile wallets, online banking, and the rise of central bank digital currencies. With trillions flowing invisibly through encrypted networks, money has evolved from

something held in hand to something trusted in code. The digital tide has swept across nearly every transaction, turning the global financial system into a vast, invisible engine powered by

data and algorithms rather than coins and bills.

Contactless payments bring a swift, seamless twist to card transactions by using Near-Field Communication (NFC) to transmit encrypted data wirelessly. These cards often house EMV chips

but skip the dip—instead, a simple tap near a compatible terminal completes the purchase in seconds. The appeal lies in speed and ease: no fumbling with slots or waiting for verification.

Despite the rapid exchange, security remains robust, as contactless systems also rely on dynamic data that’s tough to replicate. It’s a blend of convenience and protection, transforming

everyday payments into frictionless moments.

EMV chips—named after Europay, MasterCard, and Visa—revolutionized card security by embedding a microchip that generates a unique, one-time code for every transaction. Unlike magnetic

stripes that transmit static data vulnerable to cloning, EMV chips dynamically encrypt each purchase. When a card is inserted into a reader, the chip and terminal engage in a secure handshake:

the chip authenticates itself, produces a transaction-specific code, and sends it to the bank for verification. Depending on the issuer, the process may also prompt for a PIN or signature.

This layered approach makes EMV transactions far more resistant to fraud and counterfeiting.

Though chip-enabled credit cards might seem like a modern marvel, their roots stretch back to the 1980s, when France pioneered the technology with smart cards designed to outsmart

magnetic stripes. French inventor Roland Moreno laid the groundwork in the 1970s, and by the mid-1980s, banks in France and Germany were rolling out chip cards that offered enhanced

security and fraud resistance. Germany’s early patents and France’s aggressive deployment set the stage for a quiet revolution in payment systems, long before EMV chips became global

standards. While the U.S. dabbled in trials as early as 1986, widespread adoption lagged, leaving Europe to lead the charge in transforming everyday transactions into encrypted

exchanges of trust.

Origins of Smart Card Technology

1974: French inventor Roland Moreno filed the original patent for the integrated circuit (IC) card, which would later become known as the smart card.

1979: Motorola developed the first secure single-chip microcontroller for use in French banking systems.

1982–1984: France conducted field tests with chip-enabled phone cards and ATM bank cards, paving the way for broader adoption.

France Takes the Lead

1983–1984: France Telecom introduced chip cards for public payphones, marking one of the first widespread uses of smart card technology.

1988: French banks began deploying smart cards nationally, favoring them over magnetic stripe cards due to enhanced security.

Germany Follows Suit

German engineers Helmut Gröttrup and Jürgen Dethloff had already patented the smart card concept in 1968, with the patent granted in 1982.

Germany adopted chip card technology shortly after France, contributing to the development and spread of the technology across Europe.

Early U.S. Trials

In 1986, U.S. banks like the Bank of Virginia and Maryland National Bank distributed thousands of chip cards for testing, though widespread adoption lagged behind Europe.

Why Chips Matter

Chip cards—especially those using the EMV standard (Europay, MasterCard, Visa)—offer greater security than magnetic stripe cards by making data harder to clone.

Their global rollout accelerated in the 2000s and 2010s, becoming the norm for secure transactions.

For joint accounts, FDIC insurance covers up to $250,000 per co-owner, per FDIC-insured bank, meaning a joint account with two owners is insured for up to $500,000 in total.

This coverage assumes that each co-owner has equal rights to withdraw funds and that there are no other joint accounts at the same bank with the same ownership combination.

If the total balance exceeds this limit, opening additional accounts at other FDIC-insured banks can help ensure full protection of your funds.

How much money people should keep in banks depends on their financial goals, spending habits, and risk tolerance, but some widely accepted guidelines can help. Financial

experts typically recommend maintaining one to two months’ worth of living expenses in a checking account, along with a small cushion to prevent overdrafts. For savings, especially

in a high-yield account, it’s smart to set aside three to six months’ worth of expenses as an emergency fund—providing both liquidity for unexpected costs and the benefit of

earning interest. For larger balances or long-term goals, consider diversifying into certificates of deposit (CDs), money market accounts, or investment vehicles. It’s also

important to remember that FDIC insurance protects up to $250,000 per depositor, per bank, so if your balances exceed that limit, spreading funds across multiple institutions

can ensure full coverage and peace of mind.

As of July 2025, putting money in a Certificate of Deposit (CD) can be a smart move, especially for those seeking safe, fixed returns without market risk. Top CD rates

currently range from 4.25% to 4.75% APY, with short-term CDs—such as 6- or 12-month terms—offering some of the most competitive yields. While the national average for a 12-month CD

is around 1.62%, many online banks and credit unions are offering significantly higher rates. CDs are FDIC-insured, making them a low-risk option for savers who don’t need immediate

access to their funds and want to lock in a high rate before potential interest rate cuts.

High-yield savings accounts (HYSAs) are a low-risk, accessible way to grow savings, offering significantly higher interest rates than traditional savings accounts—often

exceeding 4% APY in the current market. They are ideal for short-term savings or emergency funds because they provide better returns while maintaining liquidity, allowing

customers to access their money at any time without penalties, unlike certificates of deposit (CDs). In addition to higher interest rates and flexibility, HYSAs are typically

FDIC-insured up to $250,000, making them a secure and attractive option for individuals looking to earn steady returns without sacrificing access to their cash.

Banks typically invest heavily in government bonds, which on average make up about 9% of their assets, especially in less financially developed countries. These bonds

are generally considered safe, but they carry interest rate risk—when interest rates rise, the market value of existing fixed-rate bonds falls. This inverse relationship

has become a source of concern for investors, particularly as many banks increased their bond holdings during periods of low interest rates, such as the pandemic.

As rates have risen sharply, the decline in bond values has led to unrealized losses on bank balance sheets, which can affect liquidity, capital ratios, and investor confidence.

These concerns have fueled fears that other banks may also be vulnerable to similar losses, especially if they are forced to sell these assets at a loss to meet liquidity needs.

Under the Electronic Fund Transfer Act and Regulation E, banks are generally required to reimburse customers for unauthorized electronic transactions—such as those made

by hackers—if the customer reports the issue within 60 days of receiving their bank statement. However, if the customer initiates the transfer themselves, even if they were

tricked by a scammer, the transaction may not be considered unauthorized, and the bank is not legally obligated to refund the money. That said, in some cases where a customer

is fraudulently induced into granting access, the transaction may still qualify as unauthorized depending on the circumstances. If a bank refuses to issue a refund, customers

can file a complaint with the Consumer Financial Protection Bureau (CFPB), which will forward the issue to the bank; most banks respond within 15 days, although more complex

cases may take longer.

As of 2025, the average monthly Social Security retirement benefits in the U.S. vary depending on the age at which individuals begin claiming. For those who start at age 62, the average monthly benefit is approximately $1,341.61.

At age 66, which is close to full retirement age for many, the average benefit rises to around $1,975. For those who delay claiming until age 70, the average monthly benefit increases further to about $2,002.39. These figures reflect

the impact of delayed retirement credits and the Social Security Administration’s formula, which calculates benefits based on a worker’s 35 highest-earning years, adjusted for wage inflation. Importantly, delaying benefits beyond

age 70 does not increase the monthly payout any further.

The current rate for Medicare in the U.S. is 1.45% for the employer and 1.45% for the employee, or 2.9% total; employers are also responsible for withholding the 0.9%

Additional Medicare Tax on an individual's wages

paid in excess of $200,000 in a calendar year.

Banks often invest heavily in bonds , rising interest rates have caused the price of such bonds to fail, feeding investor concerns that banks

might also be vulnerable.

Bonds have an inverse relationship to interest rates ,

when the cost of borrowing money rises (when interest rates rise), bond prices usually fall, and vice-versa.In 2023, Zelle processed approximately $806 billion in payments—nearly three times Venmo’s $275 billion—and by 2024, Zelle surpassed $1 trillion in volume with 3.6 billion transactions and 151 million enrolled users.

Despite Zelle’s claim that 99.95% of payments were completed without fraud reports, fraud losses were significant, with estimates reaching $725 million in 2023 and over $125 million in early 2024. In response to growing concerns,

the Consumer Financial Protection Bureau (CFPB) filed a lawsuit in December 2024 against Zelle and major banks like JPMorgan Chase, Bank of America, and Wells Fargo, alleging they failed to protect consumers from fraud and did not

comply with the Electronic Fund Transfer Act (EFTA) and Regulation E, which require full refunds for unauthorized transactions. The CFPB claims over $870 million in fraud losses since Zelle’s launch in 2017, while Zelle

maintains that it exceeds legal requirements and employs multilayered security to protect users.

In 2021 people sent $490 billion through Zelle , compared with $230 billion through Venmo ; and in 2020, nearly

18 million Americans were defrauded through scams involving Zelle, digital wallets and other instant payment applications, and

the 1,425 banks and credit unions that use Zelle are aware of the widespread fraud on Zelle . The Consumer Financial Protection Bureau

issued a policy required each participant institution to provide full

refunds for Zelle transactions determined to be unauthorized within the meaning of the Electronic Fund Transfer Act (EFTA) and Regulation E. Banks have to reimburse customers for losses on transfers that were “initiated by a person other than the consumer without

actual authority to initiate the transfer,” including those who obtain a victim’s device through fraud or robbery.

Zelle was created and owned by seven banks, Bank of America, Capital One, JPMorgan Chase, PNC, Truist, U.S. Bank and Wells Fargo,

to enable instant digital money transfers, and the 1,425 banks and credit unions that use Zelle can customize the app and add their own security settings. The Zelle network is operated by Early Warning Services, a company based in Scottsdale, Arizona,

responsible for manages the system’s technical infrastructure.Credit cards can often be identified by their starting digits: those beginning with 4 are Visa cards (typically 13 or 16 digits), 5 indicates MasterCard (16 digits), 6 is for Discover (16 digits), and 3 is used

by American Express, Diners Club, or Carte Blanche (usually 15 digits). A Visa card starting with 4147 is indeed valid and commonly associated with major U.S. banks, including Bank of America (Alaska Airlines Visa Signature),

Citibank (American Airlines and Singapore Airlines co-branded cards), Chase (Sapphire and Amazon Visa Signature), US Bank, Wells Fargo, and occasionally PNC Bank, Capital One, or Merrill Lynch. These 4147-prefixed cards

are part of the Visa network and often carry Visa Signature benefits.

You might have been seeing an increase in new scams involving phone calls, emails, or texts about suspicious your email account, credit card account, social security account, products, charities, medical advice and treatments, etc. Scammers often seek personal information, donations, money or gift cards to resolve urgent requests like a lawsuit,

account block or an arrest of a loved one. They may pretend to be a relative, police officer, IRS agent, FBI agent, government official, or even a hospital representative requesting payment for medical treatment. A phone call scam often threatens you and requests your personal information or bank account information. You should hang up immediately

because no bank or government official uses a phone call to request this type of information. A new text message or an email scam often alerts you that your account has been blocked, along with a link to log into your account. You should always check requests to ensure they are legitimate before taking any action. If a request is related to your

financial account, you can call your bank directly using the phone number on the back of your card for verification. You can get more information and sign up for scam alerts at FTC.gov .

A text communications from a bank typically does not show a complete phone number as the sender of the text. Shorter codes of 5 or 6 digits are usually used by a bank in the U.S. and could be displayed with or without dashes (e.g.; 410-98, 227-898, 872-265, 248487). If you see a full phone number as the sender of the text, this may be a scam.

In addition, when your bank sends an email or a text with a link to log into your account directly from the text, the email address and link will always include (yourbank).com. If you think you may have been a victim of a scam or that your personal information has been compromised, you should call the number on the back of your card (e.g.; ATM, Debit, credit card)

so your bank can assist you in securing your account.

Due to the coronavirus disease (COVID-19) pandemic, the Treasury Department and Internal Revenue Service extended the federal income tax filing due date from April 15, 2020, to July 15, 2020.

Taxpayers can also defer federal income tax payments due on April 15, 2020, to July 15, 2020, without penalties and interest, regardless of the amount owed. This deferment applies to all taxpayers, including individuals, trusts and estates, corporations and other non-corporate tax filers as well as those who pay self-employment tax.

On March 13, 2020, the White House issued an emergency declaration in response to the ongoing Coronavirus Disease 2019 (COVID 19) pandemic (Emergency Declaration). The U.S. Treasury Department and Internal Revenue Service (IRS) issued guidance allowing all

individual and other non-corporate tax filers to defer up to $1 million of federal income tax (including self-employment tax) payments due on April 15, 2020, until July 15, 2020, without penalties or interest. The guidance also allows corporate taxpayers a similar deferment of up to $10 million of federal income tax payments that would be due on April 15, 2020, until July 15, 2020,

without penalties or interest. This guidance does not change the April 15, 2020 filing deadline.

Capital One no longer offers residential mortgage loans, having exited the mortgage business in 2017–2018. It also does not provide personal loans directly, though it may refer customers to third-party lenders.

While Capital One does offer home equity loans, its offerings are limited compared to other banks. Additionally, Capital One does not provide investment or retirement account services like IRAs or brokerage accounts;

its focus remains on credit cards, checking and savings accounts, and auto loans. The bank has also been aggressively closing branches, with fewer than 500 locations remaining across eight states and D.C. as of 2025.

It closed nearly 50 branches in one quarter alone and continues to prioritize digital banking through its Capital One 360 platform3. This strategy reflects a broader industry trend toward online services, though it

has left some customers with reduced access to in-person banking.

Capital One has faced significant backlash and legal action from long-time account holders who claimed they were misled into believing their money was in high-interest savings accounts, only to receive far lower

returns than expected. The controversy centers on the bank’s decision to introduce a new account, the 360 Performance Savings, offering much higher interest rates than the older 360 Savings account—without adequately

informing existing customers of the change. As a result, many continued earning as little as 0.30% APY while new customers earned up to 4.35% APY, leading to an estimated $2 billion in lost interest. In response to

these allegations, the Consumer Financial Protection Bureau (CFPB) filed a lawsuit, and Capital One agreed to a $425 million settlement in June 2025. The incident has reinforced the perception that Capital One

prioritizes attracting new customers over supporting its existing ones.

In July 2019, Capital One disclosed a massive data breach in which the personal information of approximately 100 million Americans and 6 million Canadians—mostly credit card customers and applicants from 2005

to early 2019—was unlawfully accessed and shared with third parties. The compromised data included names, addresses, dates of birth, credit scores, self-reported income, and in some cases, Social Security and bank

account numbers. The breach was traced to a former Amazon Web Services employee who exploited a vulnerability in Capital One’s cloud infrastructure. In August 2020, Capital One agreed to pay an $80 million fine to

settle federal charges brought by the Office of the Comptroller of the Currency (OCC), which found that the bank had failed to implement adequate risk management and security controls prior to migrating sensitive

data to the cloud. The incident remains one of the largest financial data breaches in U.S. history.

In July 2012, Capital One was fined by the Consumer Financial Protection Bureau (CFPB) and the Office of the Comptroller of the Currency (OCC) for deceptive marketing practices that misled millions of customers

into purchasing unnecessary add-on products such as payment protection and credit monitoring when activating their credit cards. Investigations revealed that Capital One’s call center vendors often pressured or

misinformed consumers—particularly those with low credit scores—by implying that these products were required or would improve their credit standing. To settle the case, Capital One agreed to pay a total of

$210 million, which included $150 million in refunds to approximately two million customers, a $25 million civil penalty to the CFPB, and an additional $35 million penalty to the OCC.

When giving or receiving a gift card, it's important to understand how it works to avoid unexpected fees or loss of value. Under federal law, gift cards cannot expire for less than five years from the date of activation,

and inactivity or service fees cannot be charged unless the card has been inactive for at least 12 months—after which only one fee per month may be applied if clearly disclosed. If a gift card has an expiration date but

the funds are still available, the issuer must provide a free replacement card upon request. Additionally, some states offer even stronger protections, such as banning expiration dates or inactivity fees altogether.

If you believe a gift card issuer is not following these rules, you can file a complaint with the Consumer Financial Protection Bureau (CFPB).

Under federal law , when you apply for credit or borrow money, lenders are not allowed to discriminate against you because of race, color, religion, national origin, sex, marital status, age, and/or receiving money from public assistance. Lenders are allowed to ask you for this type of information in

some situations, but they can’t discourage you from applying for a loan or a credit card. They can’t reject your application for any of the reasons on the list — or for exercising your rights under certain consumer protection laws. Also, lenders are not allowed to charge higher costs, like a higher interest rate or higher fees, for these reasons either.

If you believe you are the victim of credit discrimination, you can submit a complaint with the Consumer Financial Protection Bureau (CFPB). Credit history is a record of your borrowing behavior, including debts, repayment history, and public records like bankruptcies or legal judgments. It begins when you open your first credit account, such as

a credit card or loan. A longer credit history—especially one with low debt and consistent on-time payments—can positively impact your credit score. FICO Scores, used in over 90% of lending decisions, typically

range from 300 to 850, though some industry-specific models may range from 250 to 900. The length of credit history accounts for about 15% of your FICO score, factoring in the age of your oldest and newest accounts,

and the average age of all accounts. While you can build a decent score in a few years, achieving excellent credit generally requires seven years of open accounts and on-time payments. Most premium credit card

offers require a strong credit profile, which takes time and responsible financial behavior to develop.

In response to the massive 2017 data breach that exposed the personal information of 147 million Americans, Equifax reached a $700 million settlement with the Federal Trade Commission (FTC),

Consumer Financial Protection Bureau (CFPB), and all 50 states. The settlement provided affected individuals with options for compensation, including up to $20,000 for out-of-pocket losses and time spent dealing with

the breach, or 10 years of free credit monitoring. Those who already had credit monitoring could opt for a $125 cash payment instead. However, to receive these benefits, individuals had to file a claim by January 22, 2020,

and those who wished to retain the right to sue Equifax independently had to opt out of the settlement by November 19, 2019. Failing to take action meant forfeiting both the compensation and the right to pursue

future legal claims against Equifax.

Since its inception in 2011, the Consumer Financial Protection Bureau (CFPB) has handled over 1 million consumer complaints from all 50 U.S. states and the District of Columbia, with the top five categories

being debt collection (27%), mortgages (23%), credit reporting (17%), credit cards (10%), and bank accounts or services (10%). These complaints highlight the most frequent financial issues faced by consumers,

including aggressive debt collection tactics, mortgage servicing problems, inaccuracies in credit reports, and disputes involving credit card charges or banking services.

While most student loan borrowers are young adults between the ages of 18 and 39, consumers aged 60 and older represent the fastest-growing segment of the student loan market. In 2015, older Americans owed

an estimated $66.7 billion in student loans, according to the Consumer Financial Protection Bureau (CFPB). This increase is driven not only by older individuals still repaying their own educational debt but

also by those who have taken out or co-signed loans to help finance the education of their children or grandchildren. As a result, many older borrowers face significant financial strain, especially as

they near or enter retirement with limited income and fewer opportunities to manage or repay this debt.

Paying for college, you may choose a student loan with some options. To be eligible for any federal student loans or grants, you need to fill out

the FAFSA form . If your aid package doesn’t cover the full cost of college, you may need to talk to your school’s financial aid office

about scholarships or alternative loan options. If you need to borrow to pay for school, federal student loans almost always cost less than private student loans and have more protections when it’s time for repayment.

Take subsidized loans first, if you are eligible. The government pays the interest on subsidized loans while you are in school. You pay the interest on unsubsidized loans. Subsidized loans are awarded to students

based on financial need. Once you agree to a federal student loan, your interest rate remains the same. Interest rates on private student loans are set by the lender and depend on the lender’s evaluation of your

creditworthiness .

A borrower who uses a five-year auto (car) loan to finance $20,000

at a 5 percent interest rate will, after three years, pay $2,190 in interest and have a remaining balance of $8,603. If the same loan is financed over six years at the same interest rate,

the borrower will pay about $2,342, which is $152 higher, in interest over the same three-year period and has a remaining balance of $10,747, which is $2,144 higher.A debt collector may file a lawsuit and win (often by default); as a result, they may be able to seize a car, home or other property after securing a court judgment. However in practice, state and federal law dramatically limit its ability to do so.

State exemption laws , which are designed to help protect income and assets from debt collectors, ensure that debtors do not become completely destitute

from the payment of debts and to preserve some small amount property for the basic necessities of living.

In 2017, there were 2,043 billionaires worldwide with a combined net worth

of $7.67 trillion, marking a significant increase of 233 individuals from the previous year. By 2024, that number had surged to a record 2,781 billionaires with a total net worth of $14.2 trillion—nearly doubling in just seven years.

This dramatic growth reflects booming tech valuations, the rise of AI-driven industries, and strong post-pandemic economic rebounds. The top billionaires in 2024 include Elon Musk ($251 billion), Bernard Arnault ($233 billion), a

nd Jeff Bezos ($194 billion), underscoring the dominance of technology and luxury sectors in global wealth creation.

As of 2025, the average credit card interest rate in the U.S. is around 23.99%, though it varies slightly depending on the source—Forbes Advisor reports 25.37%, while Federal Reserve data shows 21.91% for accounts that carry a balance.

Rates can range widely, from 0% on promotional or balance transfer offers to over 50% for subprime borrowers with poor credit, though most consumers typically see rates between 15% and 30%. This broad variability reflects differences

in creditworthiness, card types, and issuer policies.

As of December 2015, there were approximately 318 million credit card accounts in the U.S., with an average monthly spending of $2,330 per account and an average credit line of $9,060 for new customers with excellent credit.

By late 2024, the number of credit card accounts had nearly doubled to 617 million, while average monthly spending per card decreased to $1,054, reflecting more cautious consumer behavior amid higher interest rates. In 2025, average

annual credit card spending per U.S. adult exceeded $10,700, or about $892 per month, and the average credit limit for superprime borrowers rose to $12,046, indicating increased lender confidence in high-credit consumers.

Payday lenders typically charge fees ranging from $10 to $30 for every $100 borrowed, according to the Consumer Financial Protection Bureau. That means for a $500 loan, the fee could be up to $150—which aligns with your example.

If the loan is due on your next payday, usually in two weeks, the total repayment would be $650, often withdrawn automatically from the borrower's checking account. This structure results in an effective annual percentage rate (APR)

of nearly 400%, making payday loans one of the most expensive forms of borrowing.

According to survey data, 60% of credit card holders with investable assets of $100,000 or more say that cash back is their favorite credit card perk, while 22% prefer frequent flier miles. This reflects a broader trend among

affluent consumers who value the simplicity and flexibility of cash rewards over travel-specific benefits.

Your credit reports document your history of using credit, and a longer credit history generally helps your credit score. Credit scoring models like FICO and VantageScore consider the age of your oldest account, the average age

of all accounts, and how long specific accounts have been open. When you cancel an account—especially an older one—it can reduce the average age of your credit history, which may lower your credit score, particularly under scoring

models like VantageScore that may exclude closed accounts from age calculations. So, keeping older accounts open (even if unused) can be beneficial for maintaining a strong credit profile.

Credit reports and credit scores can significantly impact many areas of your financial life, including your mortgage and car loan interest rates, credit card approvals, rental applications, and in some cases, even job opportunities.

Lenders and landlords use your credit history to assess your reliability and risk, while some employers—particularly in financial or security-sensitive roles—may review your credit report (with your permission) as part of the hiring

process. That’s why it’s essential to ensure that all the information on your credit reports is accurate and up to date, as errors could negatively affect your financial and professional opportunities.

There are several situations where using a debit card is risky and best avoided. These include online shopping, where data breaches are common; purchasing big-ticket items, which are harder to dispute if something goes wrong;

and transactions requiring a deposit, such as hotel stays or car rentals, which can tie up your funds with large holds. It's also wise to avoid using debit cards at restaurants, where your card may leave your sight; with unfamiliar

or new businesses; for "buy now, take delivery later" purchases; and for recurring payments that can be difficult to cancel. Future travel bookings pose risks if plans change, and gas stations or hotels often place pre-authorization

holds. Lastly, avoid using your debit card at ATMs or checkout terminals that look suspicious, as they may be compromised by skimming devices. In all these cases, credit cards offer better fraud protection, dispute resolution,

and financial flexibility.

Swiping your debit card at certain places can expose you to significant fraud risks, with four of the riskiest being ATMs, gas stations, websites, and restaurants. ATMs—especially standalone or outdoor machines—are frequent

targets for skimming devices that steal your card information and PIN. Gas stations are similarly vulnerable due to outdated pump technology and the ease with which criminals can install skimmers. Online shopping poses risks

because debit cards offer less fraud protection than credit cards, and data breaches can compromise your account. Restaurants are also risky since your card often leaves your sight, giving dishonest employees the opportunity

to skim or copy your information. In these situations, using a credit card or a secure digital payment method is typically a safer choice.

One of the biggest retirement mistakes people make is leaving their savings in a regular bank account, where low interest rates fail to keep up with inflation. Over time, this erodes purchasing power—at an average inflation

rate of 3%, half the value of your money can disappear in about 24 years, meaning your estimate of a 50% loss every 22 years is quite accurate. While bank accounts offer safety and liquidity, they’re not suitable for long-term growth.

To protect retirement savings, money should be placed in safe, inflation-resistant investments such as Treasury Inflation-Protected Securities (TIPS), I Bonds, dividend-paying stocks, or diversified portfolios that include equities

and real estate. These options help preserve and grow wealth over time, ensuring your savings maintain their value throughout retirement.

According to recent surveys, a troubling number of Americans are unprepared for retirement, with about 45% reporting no retirement savings at all and another 19% having less than $10,000 saved—meaning roughly 64% of Americans

are expected to retire with under $10,000 in savings. Additionally, between 21% and 36% of Americans don’t contribute anything to retirement savings, depending on the survey. These figures highlight a widespread lack of financial

preparedness and underscore the importance of early and consistent retirement planning.

Your credit score is determined using a weighted formula that draws from the information in your credit report, with the most widely used models—FICO and the latest versions of VantageScore—scoring on a scale from 300 to 850.

Among these, FICO is the most commonly used by lenders, and its scoring breakdown includes: 35% based on your payment history, 30% on amounts owed (credit utilization), 15% on the length of your credit history, 10% on new

credit inquiries, and 10% on your mix of credit types. Together, these factors provide lenders with a snapshot of your financial behavior and help predict your likelihood of repaying borrowed money responsibly.

The FICO credit score ranges from 300 to 850, with the average score in the U.S. reaching 715 as of 2025. Similarly, the VantageScore now also uses the same 300 to 850 scale, aligning with FICO's range. To qualify

for a conventional mortgage, most U.S. lenders typically require a minimum credit score between 620 and 640, depending on the specific loan program and lender criteria. Private mortgage insurance (PMI) is generally available

to borrowers with scores below 660, but the cost rises as credit scores fall; for instance, those with scores between 620 and 660 may pay between 0.35% and 0.40% of the loan amount annually in PMI premiums. These credit thresholds

play a crucial role in determining both loan eligibility and the overall cost of borrowing.

As of June 2025, the average American credit card holder has about four credit cards, although individuals with higher incomes or excellent credit may carry more. Among college students, surveys show that approximately 50% to 60%

have at least one credit card, reflecting early engagement with credit but also underscoring the need for financial literacy. These trends highlight the importance of responsible credit use and education, particularly for younger

consumers who are just beginning to build their financial profiles.

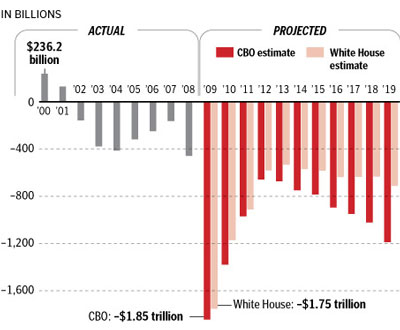

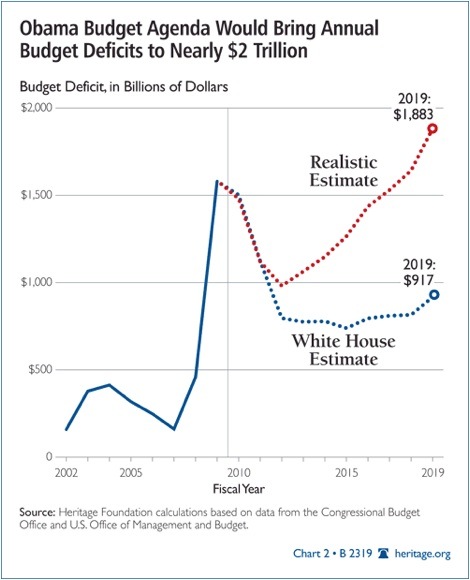

As of mid-2025, the U.S. federal government continues to rely heavily on borrowing to fund its operations. According to the Congressional Budget Office (CBO), the government borrowed $1.1 trillion in just the first seven months

of fiscal year 2025, and total federal spending is projected to reach $7.0 trillion for the year. This means that a significant portion—close to 40%—of government spending is financed through borrowing, reflecting a persistent

budget deficit and growing national debt. This trend underscores ongoing concerns about the sustainability of federal fiscal policy.

As of June 2025, around 80% of U.S. consumers owned a debit card, slightly more than the 78% who owned a credit card, while 17% reported owning a prepaid card. These figures, drawn from the Federal Reserve’s 2025 Diary of

Consumer Payment Choice, highlight the widespread adoption of electronic payment methods, with debit cards maintaining a slight lead in ownership. The data also underscores the importance of understanding the distinct features,

protections, and risks associated with each type of card.

As of 2025, approximately 214.9 million U.S. adults have a credit card account in their name, according to recent data. This marks a significant increase from previous years—up from 159 million in 2000, 173 million in 2006,

176.8 million in 2008, and 181 million in 2010—reflecting the continued growth and widespread adoption of credit cards across the country.

It is illegal for debt collectors to make empty threats about filing lawsuits or seizing someone’s home if they have no legal basis or intent to follow through. Under the Fair Debt Collection Practices Act (FDCPA),

debt collectors are prohibited from using false, deceptive, or misleading tactics to collect a debt, including threatening legal action they don’t intend to take or claiming they can seize property without proper legal authority.

Such actions violate federal law, and consumers who experience them can report the collector to the Consumer Financial Protection Bureau (CFPB), the Federal Trade Commission (FTC), or their state attorney general’s office—and

may even have grounds to sue for damages.

If you are contacted by someone who is trying to collect a debt that you do not owe, you should:

Contact your local law enforcement agencies if you feel you are in immediate danger;

Contact your bank(s) and credit card companies;

Contact the three major credit bureaus and request an alert be put on your file;

If you have received a legitimate loan and want to verify that you do not have any outstanding obligation, contact the loan company directly;

File a complaint at www.IC3.gov .

For older debts, the amount of time a collector can legally sue for payment—known as the statute of limitations—varies by state and by the type of debt, typically ranging from two to fifteen years. Once this period expires,

the debt becomes “time-barred,” meaning collectors can still attempt to collect it, but they can no longer take legal action to enforce payment. However, in some states, making a payment or even acknowledging the debt can

restart the clock on the statute of limitations, so it’s important to understand your rights before responding to old debt claims.

As of early 2025, China and Japan continue to hold the world’s largest foreign exchange reserves, with China maintaining approximately $3.2 trillion and Japan around $1.2 trillion. The Eurozone follows with about

$1.1 trillion in reserves, while the United States holds roughly $250 billion—a relatively low amount due to the U.S. dollar’s role as the dominant global reserve currency. These reserves, which include foreign currencies,

gold, and Special Drawing Rights (SDRs), are used by countries to stabilize their currencies, support trade, and manage economic shocks. While China’s reserves have declined slightly from their 2014 peak, it remains

the global leader in total reserve assets.

As of June 2025, 34% of major banks, 70% of community banks, and 78% of credit unions in the U.S. offer no-fee checking accounts to their customers, reflecting a trend toward more consumer-friendly banking options

among smaller institutions. At the same time, overdraft fees continue to be a significant source of revenue, accounting for approximately 77% of all checking account fees. This highlights the importance for consumers to

carefully review account terms and manage their balances to avoid costly penalties.

From 2020 to 2023, Wall Street bonuses fluctuated significantly in response to market conditions. In 2020, financial firms paid out approximately $31.7 billion in bonuses—a 6.8% increase from the previous year—driven

by pandemic-induced market volatility and strong trading activity. Bonuses soared even higher in 2021, marking a record-breaking year with investment bankers and traders seeing increases of 20% to 35%. However, 2022 brought

a sharp downturn, with bonuses falling by 20% to 45% across sectors, and the average bonus dropping to $176,700 from $240,400 in 2021, making it the worst bonus year since the 2008 financial crisis. In 2023,

bonuses remained flat or declined slightly overall, though some areas like equity underwriting and wealth management experienced modest gains. U.S. financial firms paid about $20.8 billion in bonus for work done in 2010.

As of 2025, the average Wall Street salary in New York City is estimated to be around $470,000, reflecting a strong rebound in profits and bonuses following a volatile few years. In contrast, the average private-sector

salary in New York City is approximately $109,601. This means that Wall Street professionals now earn more than four times the average private-sector worker’s salary in the city—slightly less than the fivefold gap seen in 2010,

when the average Wall Street salary was $361,330. The widening income disparity continues to underscore the outsized compensation structure of the financial sector relative to the broader labor market.

According to data from the Securities Industry and Financial Markets Association (SIFMA), U.S. financial firms reported approximately $180 billion in net income in 2021, $165 billion in 2022, and $157.2 billion

in 2023—amounting to more than $500 billion in profits over three years. These robust earnings were fueled by strong performance in investment banking, trading, and wealth management, even as the industry navigated headwinds

like rising interest rates, regulatory shifts, and market volatility.

A debit card may resemble a credit card in appearance, but it functions more like an electronic check. When used at a store, the card is swiped, tapped, or inserted into a payment terminal, which instantly communicates

with your financial institution to confirm that sufficient funds are available in your linked checking account. If approved, the transaction is processed and the amount is deducted almost immediately. This real-time

verification and direct withdrawal make debit cards a fast, convenient, and secure alternative to carrying cash or writing paper checks.

In November 2024, the U.S. government ran a budget deficit of $366.8 billion, collecting $301.8 billion in revenue while spending $668.5 billion—a 17% increase over the deficit recorded in November 2023.

This sharp shortfall contributed to a projected $1.8 trillion deficit for fiscal year 2025, with total federal spending expected to reach $7 trillion against $5.16 trillion in revenue. A major driver of the

growing deficit is the rising cost of entitlement programs like Social Security and Medicare, along with soaring interest payments on the national debt, which alone are projected to exceed $1.2 trillion for the year.

In November 2010, the U.S. government ran a $150.39 billion budget deficit; its income was $148.96 billion, and spending was $299.35 billion. In November 2009 the deficit was $120.29 billion

As of June 2025, the total U.S. public debt outstanding has surpassed $36.2 trillion, a dramatic increase from the $13 trillion recorded in June 2010. Meanwhile, the U.S. Treasury’s special account for public

donations to reduce the national debt—originally established in 1843—continues to receive modest contributions. In fiscal year 2022, Americans donated $180,310.32 to this fund. While more recent figures for 2025

have not yet been published, annual contributions in recent years have remained relatively small, typically ranging from $100,000 to $500,000, far below the scale needed to meaningfully impact the national debt.

As of 2025, the United States dollar (USD) is used as the official or de facto currency in several U.S. territories and independent nations. U.S. territories that use the dollar include American Samoa, Guam, Northern Mariana Islands,

Puerto Rico, and the U.S. Virgin Islands. Sovereign nations that have adopted the dollar as legal tender include El Salvador, Ecuador, Panama, Timor-Leste, the Marshall Islands, Micronesia, Palau, and Zimbabwe (which uses

multiple currencies, including the USD). Additionally, the dollar is widely used in the British Virgin Islands, Turks and Caicos Islands, and unincorporated U.S. territories such as Johnston Island, Midway Islands, and Wake Island.

In all these regions, the U.S. dollar serves as a stable and widely accepted medium of exchange.

On 1 January 1999, the European Monetary Union introduced the euro (€) as a common currency for financial institutions and electronic transactions among 11 member countries, marking its debut in non-cash form for accounting

and financial markets. Three years later, on 1 January 2002, euro banknotes and coins were officially introduced, and the euro became the sole currency for everyday transactions within the participating countries, replacing national

currencies like the French franc and Deutsche Mark in daily use.

As of 2025, the euro (€) is the official currency of 20 out of the 27 European Union member countries, collectively known as the eurozone. These countries include Austria, Belgium, Croatia, Cyprus, Estonia, Finland, France,

Germany, Greece, Ireland, Italy, Latvia, Lithuania, Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia, and Spain. While your original list reflected the early adopters of the euro, several additional

countries—such as the Baltic states, Slovakia, Slovenia, and most recently Croatia—have since joined the eurozone, expanding its reach across much of the EU.

As of 2025, seven European Union countries do not use the euro as their official currency: Denmark, Sweden, Poland, Hungary, the Czech Republic, Romania, and Bulgaria. Denmark has a formal opt-out from adopting the euro,

while Sweden has not yet met the necessary criteria and has chosen not to adopt it. The remaining countries—Poland, Hungary, the Czech Republic, Romania, and Bulgaria—are legally obligated to adopt the euro in the future

but have not yet done so, with Bulgaria expected to join next. Each continues to use its national currency, such as the Danish krone, Swedish krona, Polish zloty, and others.

As of 2025, several non-EU countries and territories use the euro (€) either officially or de facto. Microstates such as Andorra, Monaco, San Marino, and Vatican City have formal agreements with the European Union

allowing them to use the euro and mint limited quantities of their own euro coins. Montenegro and Kosovo also use the euro as their de facto currency, though without formal agreements with the EU. Additionally,

the euro is the official currency in several EU overseas territories and

Bank of America was originally founded as the Bank of Italy on October 17, 1904, in San Francisco by Amadeo Pietro Giannini to serve working-class immigrants, particularly Italian Americans, who were often underserved

by traditional banks. The bank gained prominence after the 1906 San Francisco earthquake, when Giannini famously rescued its funds and continued operations from a makeshift desk on a wharf. In 1928, the Bank of Italy merged

with Bank of America, Los Angeles, and in 1930, the combined institution officially adopted the name Bank of America. While the name change occurred in 1930, the bank’s origins trace back to its founding in 1904.

As of 2025, the number of payment cards in circulation in the United States has grown substantially since 2009. There are now approximately 827 million credit cards in use, with Visa leading the market at around

198 million U.S. cardholders, followed by MasterCard with a significant share of the remainder. Debit card usage has also surged, with about 1.2 billion debit cards in circulation nationwide, largely dominated by Visa

and MasterCard networks. American Express has around 67 million active U.S. cardholders out of 118 million globally, while Discover serves over 51 million cardholders, the majority of whom are based in the U.S.

This growth reflects the continued shift toward digital payments and the widespread adoption of credit and debit cards for everyday transactions. As of the end of 2009, there were 270 million Visa credit cards,

82 million Visa debit cards, 203 million MasterCard credit cards, 125 million MasterCard debit cards, 48.9 million American Express credit cards, and 54.4 million Discover credit cards in circulation in the United States.

The United States dollar (USD) is also commonly referred to as the American dollar or U.S. dollar, and its symbol is $. The federal government began issuing paper currency in 1861 during the Civil War to help

finance the Union’s war effort. These first notes were called Demand Notes, and they earned the nickname “greenbacks” due to their green ink. They were the first paper money issued by the U.S. Treasury for general

circulation and are considered the origin of modern U.S. currency.

The evolution of U.S. currency spans centuries, beginning in 1690 when the Massachusetts Bay Colony issued the first paper money in the American colonies. During the Revolutionary War, the Continental Congress

introduced Continental Currency in 1775. The U.S. officially adopted the dollar as its currency unit in 1785, and the Coinage Act of 1792 established the U.S. Mint and a decimal-based coinage system. In 1861,

the federal government issued its first paper currency—Demand Notes, or “greenbacks”—to finance the Civil War. The National Banking Act of 1863 standardized banknotes through nationally chartered banks.

The creation of the Federal Reserve in 1913 brought a centralized system for issuing currency, and in 1929, U.S. banknotes were standardized in size and design. The U.S. fully abandoned the gold standard in 1971,

making the dollar a fiat currency. In the 21st century, the rise of digital payments, contactless cards, and mobile wallets has continued to transform how Americans use money.

The United States Mint is responsible for producing the nation’s coins, while the Bureau of Engraving and Printing (BEP) has printed paper currency for the Federal Reserve since 1914. Originally, U.S. banknotes

were much larger in size, but in 1928, the government standardized them to the smaller, more familiar dimensions used today to reduce production costs and improve handling. As for weight, $1 million in $100 bills

weighs approximately 22 pounds, since each bill weighs about one gram and there are 10,000 bills in that amount.

All U.S. paper currency, regardless of denomination, weighs exactly 1 gram per bill, meaning $1 million in $100 bills (10,000 bills) weighs about 10 kilograms, or approximately 22 pounds. In contrast,

$1 million in $1 bills would weigh about 1,000 kilograms, or over 2,200 pounds. Coin weights vary by denomination: a penny weighs 2.5 grams, a nickel 5 grams, a dime 2.268 grams, a quarter 5.67 grams,

a half dollar 11.34 grams, and a dollar coin 8.1 grams. For example, $1 in quarters weighs about 22.68 grams—the same as $1 in dimes or half dollars—while $100 in quarters weighs roughly 2.27 pounds.

This makes high-denomination paper currency far more efficient to transport than coins or lower-value bills.

The $100,000 bill is the largest denomination of U.S. currency ever issued, printed in 1934 as a gold certificate featuring President Woodrow Wilson. It was never released to the public and was used exclusively

for transactions between the U.S. Treasury and Federal Reserve Banks as an internal accounting tool during the gold standard era. Although it technically carries the designation of legal tender, it is illegal

for private individuals to own one, and the few surviving examples are held by institutions such as the Smithsonian and the Federal Reserve for educational or display purposes only.

The issuance of high-denomination U.S. currency—specifically the $500, $1,000, $5,000, and $10,000 bills—was officially discontinued on July 14, 1969 by the U.S. Treasury and the Federal Reserve System.

The primary reasons were declining use in everyday transactions and concerns about their potential use in illegal activities, such as money laundering. Although these notes were last printed in 1945,

they remained in circulation until their formal withdrawal in 1969. Today, they are still considered legal tender, but they are extremely rare and mostly held by collectors and museums.

In 1946, the Flatbush National Bank of Brooklyn became the first bank to issue a credit card-like product through a program called “Charg-It,” developed by banker John C. Biggins. This early system

allowed local customers to make purchases at participating merchants, with the bank acting as an intermediary by reimbursing the merchants and then collecting payment from the customers. Although limited

to a small geographic area, the Charg-It program laid the foundation for the modern credit card system and marked a significant milestone in the history of consumer finance.

▷ Financial Cultures

People manage their finances through unique cultural systems—from Japan’s mindful budgeting journals to Mexico’s rotating savings circles and India’s tradition of investing in gold—each shaped

by history, values, and community norms.

Practice Region Core Idea Why It Works

Kakeibo Japan Mindful handwritten budgeting Encourages awareness and reduces impulse spending

Gold Saving India Gold as long-term wealth Stable, culturally meaningful asset

Saving Circles Philippines, Mexico Rotating pooled funds Builds discipline + community trust

Real Estate Focus China Property as security Seen as stable, long-term investment

Cash-First Germany Cash over credit Reduces overspending

Islamic Finance Middle East Interest-free, asset-backed finance Aligns with religious values

Saving with a savvy twist appears in traditions like Japan’s mindful Kakeibo and China’s community‑powered Hui, while investing with a global perspective emerges through Europe’s principled

ethical finance, the USA’s bold entrepreneurial drive, and India’s enduring gold‑based tradition; together, these practices show how each culture’s unique approach to money reflects its history,

values, and vision of prosperity.

Kakeibo budgeting becomes far more captivating when its structure flows as a single narrative: a Japanese household ledger system built around four guiding questions—how much money is available,

how much should be saved, how much is being spent, and how things can improve—all handwritten to slow the mind and sharpen awareness, while every expense falls into one of four culturally thoughtful

categories: Survival for essentials, Optional for small indulgences, Culture for books, art, and learning, and Extra for surprises; together these elements turn budgeting into a reflective ritual

that blends intention, calm, and clarity in a way that feels almost like financial meditation.

Kakeibo (家計簿) comes to life as a calm, intentional Japanese budgeting practice that turns money management into a handwritten ritual of awareness, beginning each month with goal setting,

followed by noting income and fixed costs, then tracking every purchase across categories like needs, wants, culture, and surprises through careful categorization; weekly reflection encourages

a pause to notice habits and emotional triggers, while a monthly review highlights progress and guides adjustments for the next cycle through mindful evaluation; created in 1904 by journalist

Hani Motoko, this system blends structure with mindfulness, using the slowness of handwriting to reduce impulse spending and promote intentional living, all while reflecting Japanese values

of simplicity, balance, and thoughtful daily practice.

Japan’s financial culture is defined by discipline, stability, and a deep respect for long‑term security. Households emphasize careful saving, a habit shaped by post‑war frugality and a preference

for predictable, low‑risk financial planning. Family plays a guiding role in major decisions, but individuals also take responsibility for steady budgeting and future preparation. Cash remains culturally

important despite Japan’s technological advancement, reflecting a desire for control and precision in daily spending. At the same time, retirement planning and intergenerational support drive consistent

contributions to pensions and savings accounts. Across these patterns, money functions as a tool for stability and long‑term harmony, blending tradition with a measured embrace of modern financial systems.

Gold saving in India stands out as one of the world’s most culturally rich and economically resilient financial traditions, with households holding an estimated 24,000–25,000 tons—about 11% of

global jewellery‑grade gold. Far beyond decoration, gold functions as family wealth, cultural capital, and long‑term security, appearing in weddings, festivals, inheritance, and everyday planning.

For many families—especially women—it serves as a portable, emotionally meaningful store of value and a symbol of intergenerational resilience. Economically, gold jewellery doubles as informal insurance,

offering quick liquidity through pledging or resale and acting as a hedge against inflation or limited access to formal finance. This household preference even shapes national economics: India

imported US$68.91 billion in gold from April–February 2025–26, nearly one‑tenth of all merchandise imports and over one‑fifth of the trade deficit, showing how personal saving habits can influence

macroeconomic outcomes. Across cultural, emotional, and economic layers, gold saving remains a uniquely powerful blend of heritage and practical security.

India’s money culture blends tradition, family guidance, and practical financial habits into a system built on stability and trust. Financial decisions often emerge from family and community input,

with elders offering experience‑based advice on saving, spending, and long‑term planning. Gold plays a central role as both cultural treasure and financial strategy; this gold‑saving tradition acts as

a hedge against inflation, a symbol of prosperity, and a reliable asset during emergencies. Cash remains widely used—especially in smaller towns—reflecting comfort with tangible money and a desire for

control over daily expenses. Across regions and generations, the emphasis consistently falls on saving over discretionary spending, creating a financial mindset shaped by caution, resilience, and

intergenerational wisdom.

A rotating savings circle can be elevated into a more vivid, flowing portrait: a rotating savings circle unfolds as a vibrant financial rhythm in which a group of people commits to contributing

a fixed amount at regular intervals—whether weekly, biweekly, or monthly—and each contribution joins a shared pot that goes to one member at a time, with the payout moving from person to person until

everyone has received the full lump sum, creating a cycle sustained entirely by trust rather than banks; the arrangement blends discipline with community spirit as steady contributions turn each payout

into meaningful momentum for goals such as school fees, home repairs, business ventures, or seasonal expenses, while cultural variations add their own color—Paluwagan in the Philippines, Tanda in Mexico,

Stokvel in South Africa, Susu in the Caribbean, and Arisan in Indonesia—all rooted in collective accountability, social pressure, and shared purpose; picture ten participants each contributing $100

a month to build a $1,000 pot that rotates from one member to the next until all ten have taken their turn, transforming a simple agreement into a communal financial engine that feels less like

a transaction and more like a living promise.

A Hui and a Tanda are both rotating savings circles built on trust and community, but each reflects the cultural logic of the society that created it. A Hui, rooted in Chinese communities, tends to

be more structured, often formed among relatives, coworkers, or long‑standing social networks, with contributions fixed and payout order determined by need, bidding, seniority, or mutual agreement; it

emphasizes reliability, obligation, and long‑term financial cooperation, making it a tool for major expenses like weddings, business capital, or migration support. A Tanda, common across Latin America,

is usually more informal and socially flexible, often formed among neighbors, friends, or coworkers, with a simple rotating payout order and a strong emphasis on mutual trust and community solidarity;

it serves everyday financial needs, helping participants access lump‑sum cash for bills, school costs, or emergencies. Both systems rely on social capital rather than formal banking, but the Hui leans

toward structured coordination and intergenerational financial strategy, while the Tanda reflects a more spontaneous, community‑driven approach to shared financial resilience. For deeper exploration,

comparing Hui structure and Tanda dynamics can highlight how each tradition turns trust into a financial tool.

A Chinese Hui (会) becomes far more vivid. A Hui is a trust‑driven rotating savings circle where a group agrees to contribute a fixed amount at regular intervals, creating a pooled pot

that goes to one member each cycle until everyone has received a full payout, blending financial discipline with deep social bonds; groups typically form among relatives, coworkers, neighbors, or friends,

and the payout order—whether chosen by need, bidding, seniority, or random draw—turns the process into a mix of cooperation and strategy; the system thrives because trust and obligation keep members

committed, interest‑free access to lump‑sum cash supports major expenses like weddings or business capital, and community bonding reinforces social cohesion; long used across China and in

Chinese diaspora communities worldwide, the Hui remains a resilient financial tradition that merges practicality, solidarity, and cultural continuity, standing alongside global counterparts like tandas

and paluwagan while retaining its own distinctive rhythm.

A digital Hui is the modern evolution of the traditional Chinese rotating savings circle, bringing the same trust‑based financial cooperation into apps, group chats, and online platforms while keeping

its communal spirit intact. Instead of meeting in person or collecting cash by hand, members contribute electronically at regular intervals, and the pooled amount is transferred digitally to one participant

each cycle, following a predetermined payout order. Digital Hui groups often form through messaging apps, social networks, or fintech tools, making it easier to organize participants, send reminders, track

contributions, and maintain transparency. This shift preserves the core strengths of the Hui—community trust, access to lump‑sum funds, and mutual support—while adding convenience, speed, and broader

participation, especially for diaspora communities and younger generations who prefer digital money management. In essence, the digital Hui keeps a centuries‑old tradition alive by blending cultural

continuity with modern financial technology.

China’s financial culture is shaped by a blend of tradition, discipline, and strategic long‑term thinking, creating a system where family stability and future security guide everyday money choices.

Many households rely on family‑centered financial planning, with parents and grandparents playing an active role in decisions about saving, education, housing, and major life events. A strong saving

ethic—rooted in historical scarcity and cultural values—drives high household saving rates, supported by precautionary saving habits that prioritize stability over consumption. Investments often favor

property ownership, seen as both a financial asset and a symbol of family status, while cash‑flow discipline remains central despite rapid digitalization. At the same time, China leads the world in mobile

payments, with platforms like Alipay and WeChat Pay making digital money management seamless and ubiquitous. Across these patterns, money functions as a tool for security, opportunity, and intergenerational

advancement within a culture that blends modern innovation with deeply rooted financial traditions.

South Korea’s financial culture blends rapid modernization with deep‑rooted values of discipline, education, and family responsibility. Households emphasize high saving and careful budgeting, shaped by

past economic hardship and a strong desire for long‑term security. Education is a major financial priority, with families investing heavily in tutoring and advancement, making education‑driven spending a

defining feature of household budgets. Digital payments and mobile banking are nearly universal, yet many families still rely on conservative investment choices and steady saving habits. Intergenerational

support remains central, with parents and adult children often sharing financial responsibilities. Across these patterns, money functions as a tool for stability, mobility, and family advancement in a

culture that blends tradition with one of the world’s most technologically advanced financial systems.

Vietnam’s financial culture blends family responsibility, disciplined saving, and a strong preference for stability, shaped by both tradition and rapid economic growth. Many households rely on family‑guided

financial decisions, where elders influence choices about saving, education, and major life events. A high saving ethic—rooted in historical scarcity and cultural prudence—drives consistent cash‑based saving

habits, even as digital payments expand. Property ownership and small business investment remain popular paths to security and upward mobility, while remittances from overseas relatives play a major role in

household finances. Across these patterns, money functions as a tool for stability and long‑term resilience, reflecting a culture that balances tradition with the opportunities of a fast‑modernizing

economy.

Thailand’s financial culture blends family responsibility, community support, and a growing embrace of modern digital finance. Households tend to prioritize steady saving habits, often keeping a mix of cash

reserves and bank savings to maintain stability in an economy shaped by both tradition and rapid development. Family plays a major role in financial decisions, with elders guiding choices about education,

housing, and major life events, creating intergenerational financial planning across households. Community‑based systems like informal lending circles remain common, especially in rural areas, reinforcing

trust and mutual support. At the same time, Thailand is one of Southeast Asia’s leaders in mobile payments, with platforms like PromptPay making digital money management widely accessible. Across these

patterns, money functions as a tool for stability, family resilience, and social connection within a culture that balances long‑standing traditions with fast‑growing financial innovation.

Indonesia’s financial culture blends community cooperation, pragmatism, and a strong focus on family stability. Many households rely on community‑based saving systems such as arisan—rotating savings groups

that build trust, provide liquidity, and strengthen social ties. Family plays a central role in financial decisions, with elders guiding choices about education, housing, and long‑term security, creating

intergenerational financial planning across households. Cash remains widely used, especially in rural areas, reflecting comfort with tangible money and careful budgeting, even as digital wallets and mobile

payments grow rapidly. Small business ownership and informal entrepreneurship are common paths to financial resilience, supported by disciplined saving habits and community networks. Across these patterns,

money functions as a tool for stability, social connection, and upward mobility within a culture that balances tradition with fast‑expanding modern financial systems.

A real‑estate‑focused financial culture can be captured in one vivid sweep as a mindset where households treat property as the most dependable and prestigious form of wealth, turning homeownership

into a long‑term anchor of identity, stability, and family strategy; in China, decades of rapid urbanization, limited investment channels, and strong expectations around marriage and intergenerational

support have made apartments essential assets, often purchased through pooled family resources, while in Singapore, a tightly managed housing system and government‑backed ownership programs transform